l. Introduction

Plan sponsors and other fiduciaries responsible for 401(k) plan investment menu construction, including their advisors, are demonstrating growing interest in adopting collective investment trusts (CITs) as plan investment options. There are several powerful market forces driving this trend. First, the investment strategies and related teams of investment professionals available to 401(k) plans through mutual fund complexes are becoming increasingly available through CIT structures. Second, the exemptions from registration under the federal securities laws available to CITs may afford them cost advantages relative to their mutual fund counterparts, because CITs can avoid the expenses associated with mutual fund registration, prospectus, and annual report updating and mailing, and the like. Lastly, CITs are relatively flexible arrangements. CIT structures can implement new investment strategies and approaches quickly and easily. Accordingly, banks and trust companies that offer CIT products are able to respond to market demand for customized products quickly and nimbly—particularly in the evolving target date fund segment. With all of these advantages, it is unsurprising that CITs have attracted an ever-larger percentage of 401(k) plan assets over the past 20 years.1

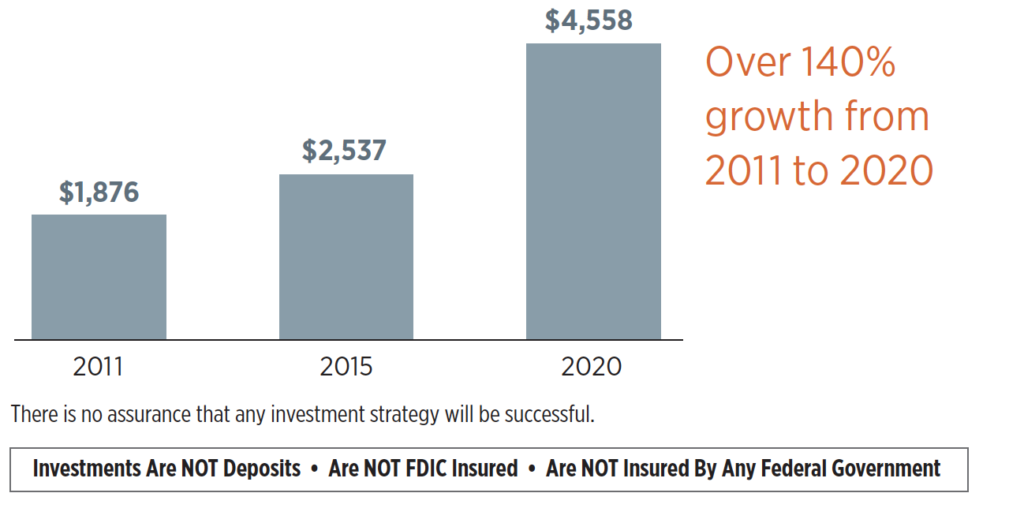

CIT assets are rapidly increasing

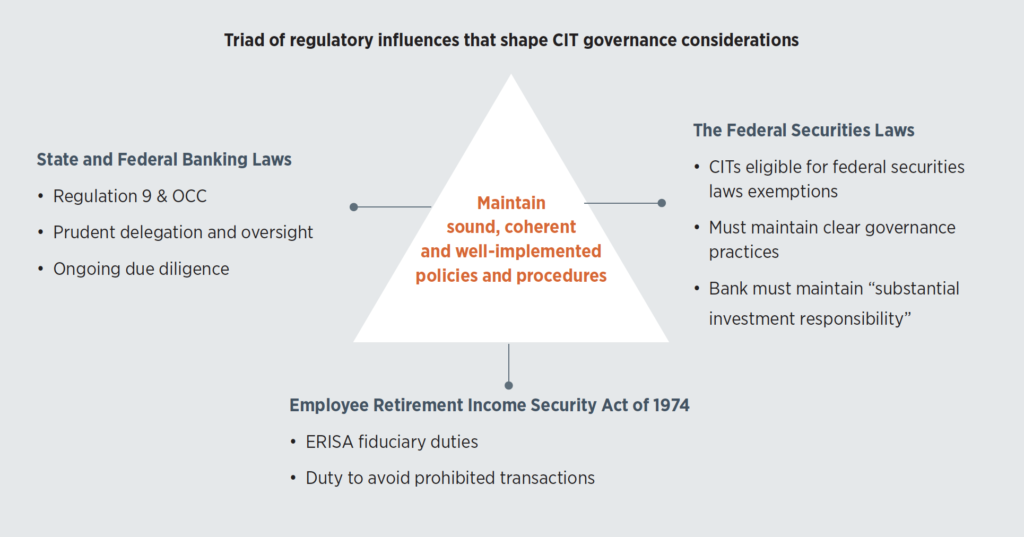

With increased interest from plan fiduciaries in CITs, the governance practices, and the policies and procedures banks and trust companies, CIT governance practices, and the policies and procedures banks and trust companies use to govern their CIT offerings, are emerging as factors that may warrant consideration by plan fiduciaries when making plan investment option decisions. As discussed below, modern CIT structures have been shaped by and reflect a triad of regulatory influences—arising, respectively, under the body of state and federal laws governing the exercise of trust powers by banking institutions; the federal securities laws; and the Employee Retirement Income Security Act (ERISA) of 1974, as amended.2 Evident in each instance is a concentrated regulatory focus on the need for

banks and trust companies that offer CITs to maintain sound, coherent, and well-implemented policies and procedures to assure that CITs are prudently administered and managed by the sponsoring institution. This paper uses the term “governance” to refer to the processes and procedures that banks and trust companies adopt for purposes of achieving these prudent CIT administration and management objectives.

Interest in good CIT governance is not limited to the community of regulators. Governance is also relevant to plan fiduciary decision-making. In this regard, a plan fiduciary’s consideration of the quality of an institution’s CIT governance practices would be consistent with undertaking a prudent evaluation of the institution’s CIT offerings.

Below, we briefly explore relevant portions under each of the three legs of the regulatory triad referenced above. In particular, we examine the regulatory emphasis on the central role that good CIT governance—in the form of well-designed and implemented bank-maintained processes and procedures—plays in the ongoing management and operation of CITs. We also address and discuss

how regulatory considerations inform CIT governance policies and may be reflected and implemented through good governance practices.

II. The Triad of Regulatory Influences That Shape CIT Governance Considerations

A. The first leg of the triad – state and federal banking laws

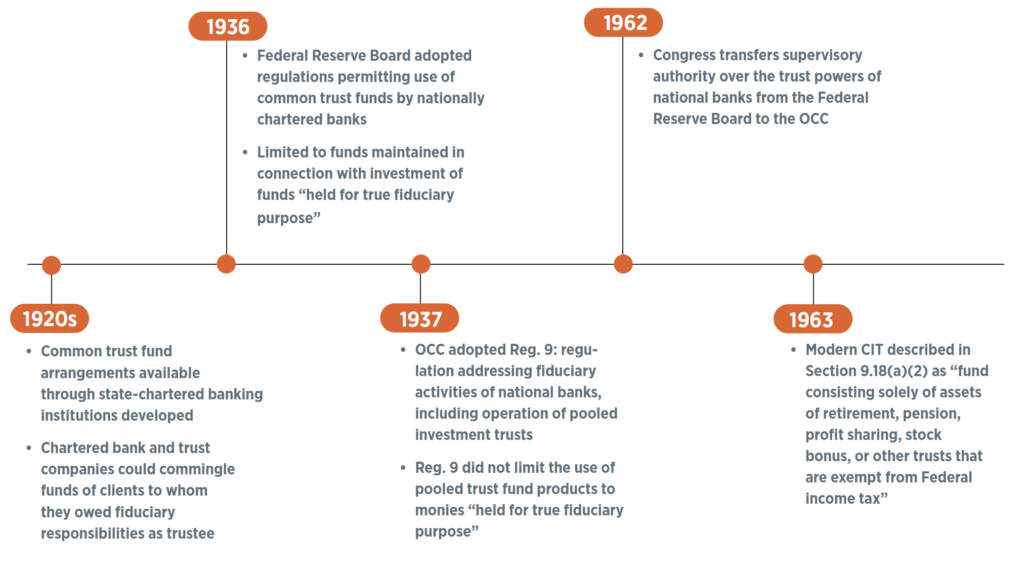

CITs of the modern era evolved from common trust fund arrangements that state-chartered banking institutions developed during the 1920s.3 It was during this period that a number of states first enacted legislation permitting state-chartered bank and trust companies to commingle funds of clients to whom they owed fiduciary responsibilities as a trustee (e.g., in connection with the administration of an estate).4 These state law developments were reflected in changes at the federal level in 1936 when the Federal Reserve Board, which at that time regulated the exercise of fiduciary powers by national banks, adopted regulations permitting the use of common trust funds by nationally chartered banks, subject to the limitation that such funds be maintained only in connection with the investment of funds “held for true fiduciary purposes.”5 The purpose of the restriction was to ensure that common trust funds maintained by national banks were used to advance economic and administrative efficiencies in the administration of fiduciary accounts, and not as vehicles for the investment of funds by the general public.6

In 1962, Congress transferred supervisory authority over the trust powers of national banks from the Federal Reserve Board to the Office of the Comptroller of the Currency (the OCC).7 One year later, the OCC adopted a comprehensive new regulation addressing fiduciary activities of national banks, including the operation of pooled investment trusts—12 C.F.R. Part 9 (Reg. 9). Importantly, Reg. 9 did not limit the use of pooled trust fund products to the management of monies held for “true fiduciary purposes.”8 This key development allowed for the emergence of modern CITs. At both the federal and state levels today, banking regulators generally look to Reg. 9 and its principles as the prevailing regulatory standard for the oversight of CITs.9

While Reg. 9 is directly applicable only to nationally chartered banks and trust companies, the laws and regulations applicable to state-chartered institutions frequently subject CITs maintained by state-chartered entities to compliance with Section 9.18 or to compliance with similarly written state provisions.10 The Federal Deposit Insurance Corporation (FDIC) recommends that “[e]ven where not required by law, the standards set forth in Section 9.18 should be followed by state nonmember banks as industry best-practices for all funds.”11

Reg. 9 distinguishes between two types of pooled trust funds. Section 9.18(a) (1) describes a traditional common trust fund as: “A fund maintained by the bank, or by one or more affiliated banks, exclusively for the collective investment and reinvestment of money contributed to the fund by the bank, or by one or more affiliated banks, in its capacity as trustee, executor, administrator, guardian, or custodian under a uniform gifts to minors act.” By contrast, the modern CIT that has emerged as a popular 401(k) plan investment vehicle is described in Section 9.18(a)(2) as: “A fund consisting solely of assets of retirement, pension, profit sharing, stock bonus or other trusts that are exempt from Federal income tax.”

Reg. 9 enshrines a core regulatory principle applicable to CIT management that profoundly shapes CIT governance considerations: “A bank administering a collective investment fund shall have exclusive management thereof, except as a prudent person might delegate responsibilities to others.”12 The OCC explains that this notion of exclusive management, subject to the ability to prudently delegate, derives from the Restatement of Trusts’ prudent investor rule.13 In guidance, the OCC has drawn similarities between the prudent investor rule’s allowance for prudent delegation and ERISA principles permitting investment fiduciaries to prudently delegate investment responsibilities.14

The OCC emphasizes that principles of prudence apply whenever a bank engages in determinations about whether and to whom CIT management authorities may be delegated:

“The trustee must act prudently in deciding whether, to whom, and in what manner to delegate fiduciary authority in the administration of a trust. The trustee should consider all relevant circumstances in connection with the delegation of investment functions, including the knowledge, skill, capabilities, and compensation of both the trustee and agent. Other circumstances to be considered include the size of the trust, the nature and complexity of the trust assets, and the particular goals of the investment strategy.”15

The OCC has also indicated that the duty of prudence is an ongoing one that continues following a decision to delegate: “The trustee is under a duty to supervise any agents to whom investment responsibilities are delegated.”16 Consistent with that guidance, the OCC has indicated, for example, that the “exclusive management” requirement of Section 9.18(b)(2) is not met if the trustee simply accepts an investor’s direction as to the broker-dealer to be used to execute a CIT’s trades.17

A national bank may use qualified personnel and facilities of affiliates to perform services related to the exercise of its trust powers; and it may, pursuant to a written agreement, purchase services related to the exercise of those powers from another bank or another third-party entity.18 But the bank’s CIT management activities remain subject to an overarching requirement—that they be managed by or under the direction of the bank’s board of directors, even though the board may permissibly assign any function related to the exercise of fiduciary powers to a bank director, officer, employee, or committee.19

It has become increasingly commonplace for banks to engage the services of expert investment advisors—typically referred to as “subadvisors”—to render recommendations to the bank with respect to the investment and re-investment of CIT assets. As noted at the outset of this paper, part of the appeal of CITs to plan fiduciaries is that the strategies and the investment personnel utilized by CIT subadvisors often align with those of a counterpart, previously established, mutual fund offering. By adopting CITs, a plan may make those same strategies and investment personnel available to participants, but at a relatively lower level of expense. The activities of the CIT subadvisor, however, remain subject to the oversight and ultimate authority of the bank.

With respect to the use of subadvisors, a particular OCC concern is that banks not “rent their charters” to third-party registered investment advisors seeking to use the bank’s status as a fiduciary to sponsor one or more funds on their behalf.20 The OCC has emphasized that a bank’s use of outside third parties to perform functions on its behalf does not diminish the responsibility of the bank’s internal management team to ensure that those functions are performed in a safe and sound manner and in compliance with applicable laws.21 The OCC expects a national bank relying upon third parties, including CIT subadvisors, to maintain risk management processes that are commensurate with the level of risk and complexity of the third-party relationship; with more comprehensive and rigorous oversight and management of third-party relationships that involve critical activities.22 Accordingly, the OCC expects that banks utilizing the services of CIT sub-advisors will exercise periodic reviews of sub-advisor performance, style consistency, and investment of fund assets in a manner consistent with applicable investment guidelines.23

National banks are required to adopt and follow written policies and procedures that are adequate to maintain their fiduciary activities in compliance with applicable law.24 The OCC has offered suggestions on risk management and on the development, implementation, and use of risk management procedures.25 Under that guidance, a bank should be able to demonstrate control over the documents that afford clients access to CIT investment funds, including the maintenance of original documentation in a secure, centrally controlled location. The bank also should maintain a system of internal controls, including an effective audit program for assuring that the bank is adhering to the terms and conditions of CIT instruments (i.e., declarations of trust and participation agreements).26

A national bank also is required to conduct a formal review of all of the assets

for which it has investment discretion at least once per year.27 The review must determine whether CIT assets are being invested in a manner consistent with the fund’s plan and investment strategy.28 It should also reflect deliberation on the fund’s investment objectives and guidelines and investment performance, as well as reaffirm or change the investment objectives and guidelines as appropriate.

TO SUMMARIZE: Reg. 9 and the OCC’s related guidance emphasize the importance of ongoing bank monitoring and oversight of CIT functions, including oversight of any services of subadvisors and other vendors as an essential element of maintaining CITs. The trustee of a CIT may not function as a mere custodian, but needs to undertake active, ongoing due diligence and inquiry as to whether the needs of the CIT are being met and whether the interests of the CIT are being properly served. As noted, the principles of Reg. 9 are looked to by regulators, including the FDIC, as “best practices” for CITs maintained by state-chartered institutions.

B. The second leg of the triad – the federal securities laws

Sections 3(c)(11) of the Investment Company Act of 1940 (the ’40 Act) and 3(a (2) of the Securities Act of 1933 (the ’33 Act) make available to CITs counterpart exemptions from the registration and related disclosure and reporting requirements under each of those statutes. In order to qualify for the exemptions, CITs must be “maintained by a bank” and must consist solely of assets of one or more trusts of certain types of retirement plans—primarily those that meet qualification requirements under Code section 401(a), certain types of governmental plans or church plans.29

The Staff of the Securities and Exchange Commission (SEC) has stated that it would not be inconsistent with the “maintained by” requirement for a bank to retain an investment advisor to assist with the management of CIT assets.30 However, the Staff has made clear that a bank may not go so far as to entirely out-source CIT investment management responsibilities by relying completely on the efforts of a retained investment advisor. In the view of the SEC, the key phrase embedded within the exemptions—referencing CITs that are “maintained by a bank”—requires a bank relying on the exemptions to exercise “substantial investment responsibility” over CIT assets; a bank that functions in a mere custodial or similar capacity with respect to CIT assets fails to satisfy the requirement.31 In no-action letter guidance, the SEC Staff has indicated that a bank relying upon the recommendations of third-party investment advisors for purposes of managing CIT assets would need to approve or authorize those investment decisions contemporaneously or in advance to demonstrate the exercise of substantial investment responsibility.32

The emergence of modern CITs

The Frank Russell no-action letter referenced in footnote 32 describes an approach to CIT investment management that is widely used today. There, the bank maintaining CITs indicated its intent to retain the services of one or more investment advisors to furnish it with advice and recommendations concerning the specific securities to be purchased and sold by CITs. The bank indicated it also intended to utilize consulting services provided by a non-bank affiliate to identify and evaluate the investment advisors that it might choose to engage. Importantly, while the bank indicated it expected to rely upon the recommendations furnished by these investment advisors and consultants, it represented that it would retain complete discretion to accept or reject that advice. The bank also represented that it would maintain staffing levels appropriate for making those determinations. In granting the requested no-action relief, the SEC Staff expressed the view that the approach would satisfy the “maintained by a bank” requirement under the Section 3(c)(11) and 3(a)(2) exemptions because the bank’s use of staff to oversee and to accept or reject the input of third-party advisors would involve an exercise by the bank of “substantial investment responsibility” over the CIT.33

In a 2006 SEC enforcement proceeding involving a common trust fund claiming exemption from registration under section 3(c)(3) of the ’40 Act (which contains an identical “maintained by” requirement), the SEC concluded that the requirement would not be satisfied where a trust fund served as an intermediary vehicle for investors to indirectly invest in privately offered investment funds that were unavailable for direct investment.34 In that case, the SEC expressed the view that the bank did not truly “maintain” the common trust fund but was merely a directed investment arrangement because investors in the fund instructed the trustee as to the ultimate investment of the common trust fund into underlying private investment vehicles.

More recently, in 2020 the SEC determined that a trustee failed to satisfy the

“maintained by” requirement for both its common trust and collective trust funds.35 In that case, the trust company sponsoring the funds relied upon the services of an affiliated investment advisor to assist with the management of the funds. The SEC faulted the trust company for engaging in only minimal oversight of its investment advisor affiliate, alleging that the advisory affiliate performed virtually all investment activities on behalf of the funds, including investment due diligence, investment selection, purchase and sales activities, and monitoring for performance and risk. The SEC also noted that the trustee’s oversight of its advisor affiliate was “cursory,” largely limited to the passive receipt of information and reports submitted by the advisor and rarely resulted in any investment changes or feedback to the advisor in respect of the funds’ investment strategy.36.

TO SUMMARIZE: The federal securities laws compliance needs for well-designed and implemented CIT governance practices are clear and unmistakable—CITs are “maintained by a bank” and therefore eligible for the federal securities laws exemptions that may allow for cost savings relative to mutual funds, only where the bank exercises substantial investment authority, including through subadvisor oversight and contemporaneous or advance approval of subadvisor recommendations.

C. The third leg of the regulatory triad – ERISA

ERISA assigns fiduciary responsibilities to persons who engage in certain functions, including to persons who exercise authority or control over the management or disposition of the assets of an ERISA-covered plan.36 Trustees to ERISA-covered plans are always fiduciaries.37

Under U.S. Department of Labor (DOL) regulations, where an ERISA-covered plan acquires or holds an investment interest in a common or collective trust fund of a bank, the assets of the plan include both an investment interest in the trust itself and an undivided interest in each of the underlying assets of the trust.38 Accordingly, whenever a CIT admits one or more ERISA-covered plans as an investor, that CIT instantly becomes an ERISA “plan assets vehicle.” Consequently, the CIT trustee is responsible as an ERISA fiduciary to each such participating plan. This contrasts with the ERISA treatment of mutual funds, which are not plan assets vehicles. Therefore, those who are responsible for the management of a mutual fund’s asset portfolio, including the mutual fund’s investment advisor, are not responsible as ERISA fiduciaries to plans that invest in the mutual fund.

- ERISA fiduciary duties

ERISA section 404 imposes standards of conduct on persons who act

as fiduciaries. These general fiduciary responsibility provisions include requirements that the fiduciary act prudently, solely in the interest of plan participants and beneficiaries, and for the exclusive purpose of paying benefits under the plan and defraying reasonable expenses.40 We discuss these responsibilities in more detail below.

a. Duty of prudence

ERISA fiduciaries must act “with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent man acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.”41 In considering whether a fiduciary has acted in a manner that satisfies the duty of prudence under section 404, courts generally focus on the fiduciary’s conduct in arriving at a decision, not on the decision’s results. In this regard, courts frequently inquire as to whether a fiduciary used appropriate methods to investigate and determine the merits of a particular decision.42 Whether a fiduciary acted prudently depends on “whether the fiduciary engaged in a reasoned decision-making process, consistent with that of a prudent man acting in a like capacity.”43

The DOL has indicated that a fiduciary’s obligation to carry out its duties “prudently” is generally met to the extent that the fiduciary follows a “procedurally prudent” process by (i) gathering relevant information, (ii) considering all available courses of action, (iii) consulting experts where appropriate, and (iv) making a reasoned decision based on all relevant facts and circumstances. Such a process should be designed to avoid self-dealing, conflicts of interest, or other improper influence.44

A fiduciary may choose to obtain independent financial or legal advice to assist it in managing its responsibilities. Some courts have indicated that the act of seeking out such advice is demonstrative of having undertaken a prudent and thorough investigation.45 However, most courts have regarded the mere act of obtaining advice from an independent advisor as insufficient, in and of itself, to establish that a fiduciary acted prudently.46

b. Duty of loyalty

ERISA’s fiduciary duty of loyalty requires plan fiduciaries to act for the

“exclusive purpose of providing benefits to participants and beneficiaries; and defraying reasonable expenses of administering the plan.”47 This duty of loyalty has been described to require that fiduciaries act with an “eye single” to the interests of plan members and beneficiaries and without regard to the interests of any other persons.48 However, a fiduciary action that “incidentally benefits” the interests of the fiduciary itself does not violate the exclusive purpose rule where the fiduciary reasonably concludes, following prudent inquiry, that the action is in the best interests of the plan participants and beneficiaries.49 A recent court decision noted that a fiduciary’s adherence to a demonstrably prudent decision-making process provides an inference that that ERISA fiduciary’s motive was to act “in the interest of the participants.”50

2. Duty to avoid prohibited transactions

The general fiduciary responsibility requirements of ERISA are supplemented by rules restricting fiduciaries from causing a plan or a plan assets vehicle from engaging in “prohibited transactions.” In general, under ERISA, most transactions involving related parties are prohibited unless an applicable statutory or administrative exemption applies. The prohibited transaction rules are contained in two parts: the party-in-interest restrictions under ERISA section 406(a), and the fiduciary self-dealing and conflict-of-interest prohibitions under ERISA section 406(b).

ERISA section 406(a) prohibits a fiduciary from causing a plan to engage in a transaction if the plan fiduciary knows or should know that the transaction will involve, directly or indirectly, one or more of certain categories of transactions with a “party in interest.” The term “party in interest” includes fiduciaries, service providers, employers of plan participants, corporations that are 50-percent owned by a party in interest, and employees, officers, directors, and 10-percent owners of certain parties in interest.51

Specific transactions prohibited by ERISA section 406(a) include a sale or exchange of property between a plan and a party in interest; a lending or extension of credit between a plan and a party in interest; the provision of services by a party in interest to a plan; and the transfer to, or use by or for the benefit of, a party in interest of any assets of the plan.

ERISA section 406(b) generally prohibits a fiduciary from acting under a conflict of interest. ERISA section 406(b)(1) prohibits a plan fiduciary from dealing with plan assets in the fiduciary’s own interest or for the fiduciary’s own account. ERISA section 406(b)(2) prohibits a fiduciary from acting on behalf of a party whose interests are adverse to the interests of the plan or its participants in a transaction involving plan assets. ERISA section 406(b)(3) prohibits a fiduciary from receiving consideration for its own personal account from any party dealing with the plan in connection with a transaction involving plan assets. The DOL has explained that a violation of ERISA section 406(b) will occur when a fiduciary uses the authority, control, or responsibility that makes the person a fiduciary in a transaction where the fiduciary has interests that may affect its best judgment as a fiduciary.52

TO SUMMARIZE: Under ERISA, banks that maintain CITs are responsible as fiduciaries when they manage the assets of those plans. As such, banks are required to manage those assets prudently, solely in the interests of the plans, and in a manner that avoids giving rise to a non-exempt prohibited transaction. While the common practice of engaging one or more expert investment advisors to assist the bank in its management role is consistent with the principles of prudence, it is insufficient, in and of itself, to discharge that duty. Consistent with the duties of prudence and loyalty that ERISA imposes, where a fiduciary relies upon an expert, including a subadvisor, it is obligated to evaluate and consider the expert advice and recommendations that it receives, including the qualifications of the provider(s) of that advice. Such a process would also seek to avoid non-exempt prohibited transactions. Well-governed bank CITs apply these principles by engaging in regular oversight of expert subadvisors and of their recommendations and by taking appropriate steps to ensure ongoing compliance with applicable prohibited transaction exemptions.

Demonstrating prudent oversight through solid CIT governance

III. Demonstrating Prudent Oversight Through

Good CIT Governance

As noted above, this paper uses the term “governance” to refer to the policies and procedures banks and trust companies may utilize for purposes of overseeing and authorizing decision-making on behalf of CITs. Good governance is the means by which CIT trustees demonstrate adherence to the active due diligence and prudent oversight principles that are a thematic focus under each leg of the regulatory triad.

While there are a number of governance approaches available, the decision on which approach to use partially depends on the facts and circumstances of each financial institution that sponsors CITs. Whatever the approach to governance, the overriding regulatory directives that some appropriate governance be maintained under each leg of the regulatory triad described above is clear.

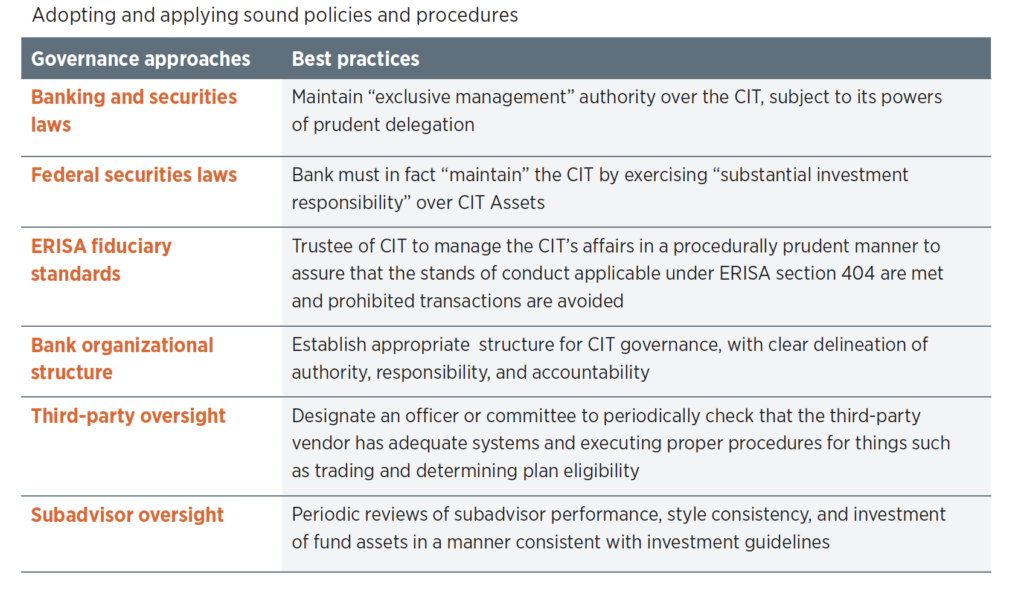

First, as a matter of federal banking regulation, the OCC has made clear that the bank, through its board of directors and the board’s assigned directors, officers, employees or committees, must maintain “exclusive management” authority over all CITs, subject to its powers of prudent delegation; state banking regulators generally conform to the OCC’s rules. Second, for purposes of maintaining compliance with applicable exemptions from registration under the federal securities laws, the bank must in fact “maintain” the CIT by exercising “substantial investment responsibility” over CIT assets. Third, as an ERISA fiduciary, it is incumbent upon the CIT trustees to manage the affairs in a procedurally prudent manner to assure that the standards of conduct applicable under ERISA section 404 are met and that non-exempt prohibited transactions are avoided.

The OCC does not prescribe a one-size-fits-all approach to governance. Instead,

it notes that governance structures and practices should keep pace with changes in size, risk profile, and complexity relevant to a financial institution and its businesses.53 Typically, the bank’s board of directors establishes an appropriate organizational structure for CIT governance, with clear delineation of authority, responsibility, and accountability.

Many, if not most, financial institutions choose to implement a committee structure for CIT oversight purposes. These oversight committees approve and implement policies and procedures, including policies and procedures for selecting and monitoring subadvisors. Committees may also establish subgroups, or subcommittees, charged with specific areas of responsibility.

The authorities assigned to a committee are typically outlined in a charter document that would preferably afford some level of flexibility for the delegation of responsibilities. Ideally, delegations should be appropriately documented to make clear that the committee has selected a delegate to act on its behalf for a specific function. Documentation should also define the scope and extent of the delegated functions and be executed by both the committee and the delegate. After a committee has been established, it should meet on a regular basis and maintain meeting minutes to document its decision-making process.

A critical aspect of good fiduciary governance is ensuring that CIT fiduciary oversight functions have been specifically assigned to one or more designated committees, subcommittees and/or delegated personnel—and that those designees or delegees are actively performing the oversight functions for which they are responsible and regularly reporting back. This involves periodic checking by the bank’s senior management to make sure that those responsible for CIT governance are fully informed about the specific oversight functions arising under applicable law; have taken the necessary steps to ensure that those specific oversight functions have been assigned; and that the personnel responsible for those assignments are actually performing the assigned functions. While a complete description of all oversight functions applicable to CIT governance is beyond the scope of this paper, we have listed several key fiduciary oversight items below.

As noted, Reg. 9 provides that a national bank may use qualified personnel and facilities of affiliates to perform services related to the exercise of its fiduciary powers. The OCC has emphasized that such personnel need to be qualified and competent, and should perform appropriately.54 They must also comprehend the bank’s mission, values, principles, policies, and practices.55 A national bank may also, pursuant to a written agreement, purchase services related to the exercise of fiduciary powers from another bank or other entity.56 However, the use of third-party services in connection with the operation of CITs remains subject to meeting the “exclusive management” requirement under section 9.18(b)(2). To the extent third parties are being utilized, the governance structure should assign or otherwise make provisions for overseeing those vendors for purposes of assuring that they are conducting their services in a sound manner and in compliance with applicable law.

For example, if CITs rely on third-party intermediaries to serve as conduits between participating plans and the bank, an appropriate governance mechanism would be to designate an officer or committee to periodically check that the third-party vendors have adequate systems in place to assure that only eligible plans are admitted to participate in CITs. Similarly, periodic checks should be made to assure that third-party vendors are executing CIT admissions and withdrawals on a timely basis, monitoring trading activity to guard against “late trading” and “market-timing” abuses, and correctly assessing and collecting fees. The appropriate officer or committee should document that these checks have taken place.

With respect to the use of subadvisors, we have noted above that the OCC is concerned that banks not “rent their charters” to third-party registered investment advisors seeking to use the bank’s status as a fiduciary to sponsor one or more funds on their behalf.57 Periodic reviews of subadvisor performance, style consistency, and investment of fund assets in a manner consistent with applicable investment guidelines would be consistent with the prudent exercise of oversight responsibilities. These reviews should be documented in meeting minutes, written reports, or both. The bank’s governance structure should assign responsibility for regular comparisons of subadvisor performance to benchmarks to the appropriate officers or committee members. The structure should also assign responsibility for supervising and being able to describe how an appropriate benchmark was selected.

As a matter of federal securities law compliance, it is critical that the bank’s governance process provide for ongoing receipt and review of subadvisor trades, consistent with its obligation to exercise substantial investment responsibility over CITs. It would be consistent with sound governance to contemporaneously review the trades for consistency with CIT’s investment guidelines, to make sure they are not otherwise imprudent and to take appropriate steps to set aside or reverse problematic trades should they arise.

The focus on process and procedure that comes with good CIT governance is consistent with adherence to the ERISA duty of prudence, which has a strong process orientation. In addition, and as noted, adherence to a rigorous oversight process is also useful in demonstrating adherence to the ERISA duty of undivided loyalty, as well as in monitoring for compliance with applicable prohibited transaction exemptions.

A sound governance structure involves identifying the ERISA-prohibited transaction exemptions relied upon by CITs, assuring that the scope of relief afforded by the exemptions is sufficient to cover necessary CIT transactions, and that the CIT is meeting applicable conditions for relief. Where a subadvisor or another third party is responsible for prohibited transaction exemption compliance, good governance would seek to apply an appropriate level of oversight over such third-party’s compliance.

In conclusion, adopting and applying sound policies and procedures for CIT governance is a regulatory imperative for banks that act as CIT trustees. Good governance practices are also protective of CIT investor interests by helping to assure that CIT investment objectives are being advanced in an appropriate manner. In light of that protective function, 401(k) plan sponsors, advisors, and other plan fiduciaries may wish to inquire about CIT governance practices when evaluating CITs as potential plan investment options.

This article is for informational purposes only and is not intended as an offer or solicitation for the sale of any financial product or service. This article is not designed or intended to provide financial, tax, legal, investment, accounting, or other professional advice since such advice always requires consideration of individual circumstances. If professional advice is needed, the services of a professional advisor should be sought. There is no assurance that any investment strategy will be successful.

1 In 2019, total CIT assets exceeded $3.78 trillion and the share of 401(k) plan assets invested reached 30.1%, or approximately $1.94 trillion. The Cerulli Report U.S. Defined Contribution Distribution 2020: Adapting to Changes in the Regulatory Environment.

2 The Internal Revenue Code (Code) has also exerted a strong influence on the development of CITs. Federal tax laws have largely focused on the types of arrangements eligible to participate in CITs as distinct from the governance processes and procedures a sponsoring financial institution utilizes to manage CITs.

3 W. Wade, Bank-Sponsored Collective Investment Funds: An Analysis of Applica-ble Federal Banking and Securities Laws, 35 Bus. Law. 361, 363 (1980).

4 Please also note: as used in this article, the word “bank” refers to both depository institutions regulated as such and to trust companies. Trust companies are business entities authorized to engage in the business of acting as a trustee and similar fiduciary and custodial activities. Although regulated as banking institu-tions, trust companies typically do not engage in the typical commercial banking functions of accepting general deposits and lending money. See, W. Wade, Bank-Sponsored Collective Investment Funds: Multi-Dimensional Regulation, First Edition, published by the American Bankers Association, (2015).

5 Wade, 35 Bus. Law. 361,364.

6 Id., citing 26 Fed. Res. Bull. 393 (1940).

7 Id., at 365.

8 Id.

9 See FDIC Trust Examination Manual, Section 7, Compliance- Pooled Investment Vehicles (many states have promulgated laws regarding CIFs. Due primarily to the need to comply with federal securities and tax laws, state laws are generally similar to Regulation 9.18.)

10 FDIC Trust Examination Manual, Section 7, Compliance- Pooled Investment Vehicles, Section 7.E.1.

11 Id.

12 C.F.R. § 9.18(b)(2) (emphasis added).

13 See Comptroller’s Handbook, Asset Management, Collective Investment Funds, Version 1.0 (May, 2014), at 43.

14 See Comptroller’s Handbook, Investment Management Services (Aug. 2001), at 120.

15 Id.

16 Id.

17 OCC Interpretive Letter No, 219 (May 25, 1989).

18 12 C.F.R. § 9.4.

19 Id.

20 See OCC Bulletin 2011-11, Collective Investment Funds and Outsourced Arrangements (a bank’s delegation of its responsibilities to a third party does not relieve the bank of its responsibilities as a fiduciary) and OCC Bulletin 2020-10, Third-Party Relationships: Frequently Asked Questions to Supplement OCC Bulletin 2013-29 (March 5, 2020).

21 See OCC Bulletin 2013-29, Third-Party Relationships: Risk Management Guidance (Oct. 30, 2013).

22 Id.

23 See Comptroller’s Handbook, Investment Management Services (Aug. 2001), at 25.

24 12 C.F.R. § 9.5.

25 OCC Bulletin 2011-12, Sound Practices for Model Risk Management: Supervisory Guidance of Model Risk Management.

26 Id.

27 12 CFR §9.6.

28 See Comptroller’s Handbook, Asset Management, Collective Investment Funds, Version 1.0 (May 2014), at 19.

29 The ’40 Act defines the term “bank”

in section 2(a)(5) to include depository institutions as defined under the Federal Deposit Insurance Act, a Federal Reserve System member bank and “any other banking institution or trust company … doing business under the laws of any state of the United States, a substantial portion of the business of which consists of receiving deposits or exercising fiduciary powers similar to those permitted to national banks under the authority of the Comptroller of the Currency and which is supervised or examined by State or Federal authority having supervision over banks … .” The ’33 Act’s section 3(a)(2) exemption incorporates the same’40 Act definition by reference.

30 First Liberty Real Estate Fund, SEC No- Action Letter (July 14, 1975).

31 See, Employee Benefit Plans, Securities Act Rel. No. 6188 (Feb. 1, 1980).

32 See, e.g., Frank Russell Trust Co., SEC No-Action Letter (July 11, 1980).

33 Id.

34 In re Dunham & Associates, Inc., SEC Securities Act Rel. No. 8740 (Sept. 22, 2006).

35 Great Plains Trust Company, Inc., SEC Release No. 33-10869, 2020 WL 5820419 (Sept. 30, 2020).

36 ERISA § 3(21)(A)(i).

37 29 C.F.R. § 2509.75-8.

38 29 C.F.R. § 2510.3-101(h)(1).

39 Section 401(b)(1) of ERISA excludes a mutual fund’s underlying holdings from plan assets treatment. It provides—“in the case of plan which invests in any security issued by an investment company registered under the Investment Company Act of 1940, the assets of such plan shall be deemed to include such security but shall not, solely by reason of such investment, be deemed to include any assets of such investment company.”

40 ERISA § 404(a)(1)(A), (B).

41 ERISA § 404(a)(1)(B).

42 See, e.g., In re Unisys Savings Plan Litiga-tion, 74 F.3d 420, 434 (3d Cir. 1996).

43 See DiFelice v. U.S. Airways, Inc., 497 F.3d 410, 420 (4th Cir. 2007); see also Eyler v. Comm’r of Internal Revenue, 88 F.3d 445, 454 (7th Cir. 1996) (a court must consider whether a fiduciary “employed the appro-priate methods”).

44 DOL Field Assistance Bulletin 2003-02 (Nov. 22, 2003).

45 See, e.g., Chao v. Hall Holding Co., 285 F.3d 415, 430 (6th Cir. 2002); Howard v. Shay, 100 F.3d 1484, 1489 (9th Cir. 1996).

46 Martin v. Feilen, 965 F.2d 660, 670

(8th Cir. 1992) (securing an independent assessment from a financial advisor or legal counsel is not a complete defense to a charge of imprudence); DiFelice v. U.S. Airways, Inc., 2007 WL 2192896 at *8 (4th Cir. 2007) (although plainly independent advice provides evidence of a thorough investigation, it is not a “whitewash”).

47 ERISA § 404(a)(1)(A).

48 Donovan v. Bierwirth, 680 F.2d 263, 271 (2d Cir.), cert. denied, 459 U.S. 1069 (1982).

49 Id., at 271.

50 Rozo v. Principal Life Ins. Co., No.

4:14-cv-00463-JAJ, 2021 WL 1837539, at *20 (S.D. Iowa Apr. 8, 2021).

51 ERISA § 3(14).

52 29 C.F.R. § 2550.408b-2(e).

53 Comptroller’s Handbook, Safety and Soundness, Corporate and Risk Governance Version 2.0 (July, 2019) at 1.

54 Comptroller’s Handbook, Asset Man-agement, Collective Investment Funds, Version 1.0 (May, 2014), at 32 (emphasizing the need for national banks to attract, develop, and retain appropriately qualified personnel).

55 Id.

56 12 C.F.R. § 9.4.

57 See OCC Bulletin 2011-11, Collective Investment Funds and Outsourced Arrangements (a bank’s delegation of its responsibilities to a third party does not relieve the bank of its responsibilities as a fiduciary).