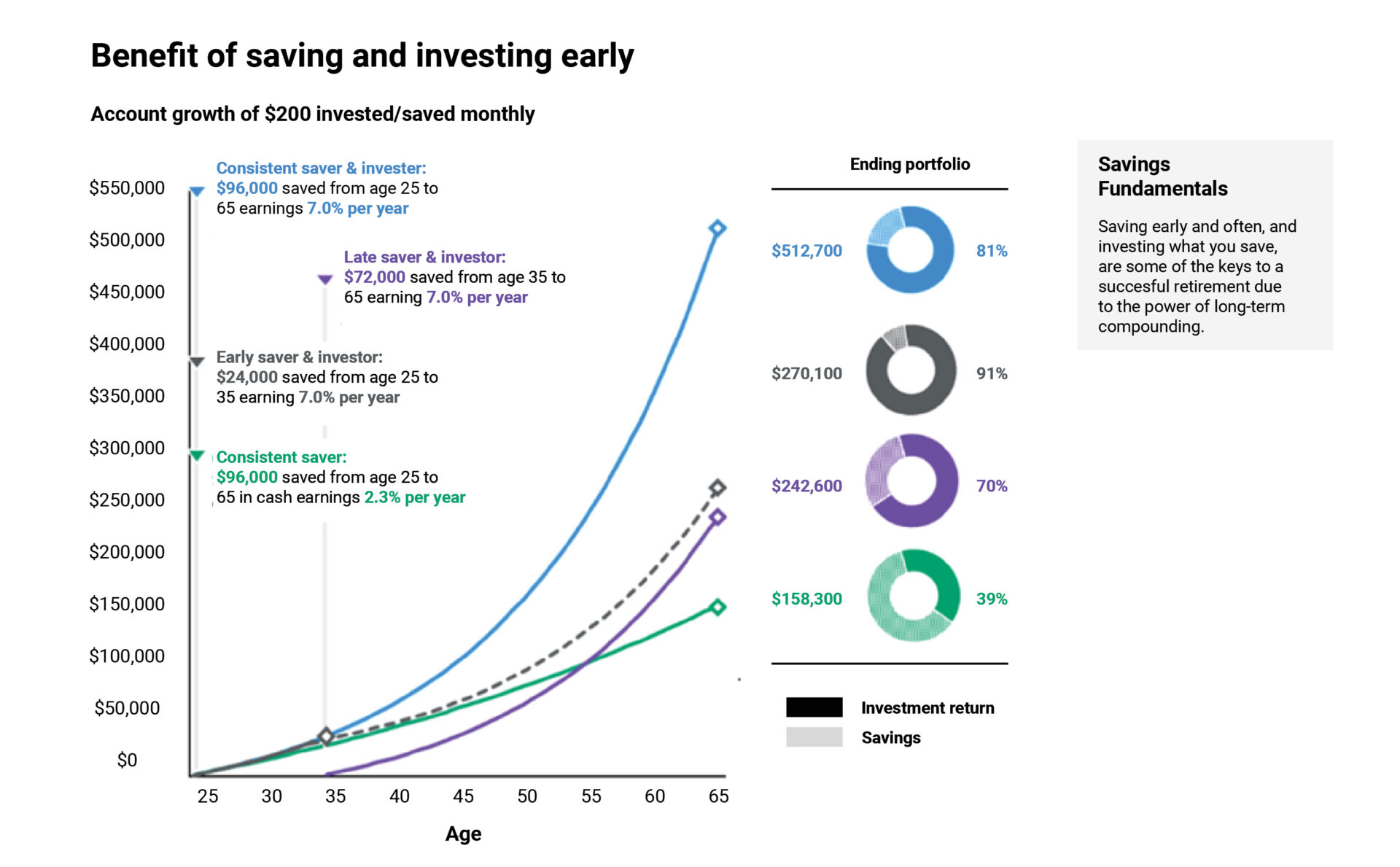

The early bird really could get the worm! In the chart below you will find no secret tips or tricks to investing that cite prior market events: just plain old math.

Download a copy of this Participant Corner by clicking here, or contact service@accelerateretirement.com to get an editable version that you can white label and distribute.

The amount of your total nest egg is exponentially influenced by the duration of time it has to compound. In other words, the earlier you start saving, the better, by leaps and bounds. Of the four scenarios, please focus on the two profiles in the middle. The “early saver & investor” invests ($200/month) for only 10 years, while the “late saver & investor” saves ($200/month) for 30 years. Both portfolios earn the same amount in this example (7%), but the early saver has a higher amount at retirement by nearly $30,000!

Of course, we all want to be the “consistent saver & investor,” and there is much to be said about the importance of staying invested for the long term. However, as some have been told when beginning their working career, it’s not about “timing the market,” but much more about “time in the market.”

Chances are that you are already on a path of saving for your retirement or playing a little catch up. That does not preclude you from stressing the importance of saving to all your younger colleagues, family, and friends! The math shows that individuals could be significantly better off starting as early as possible.

Source: J.P. Morgan Asset Management, Long-Term Capital Market Assumptions.

Individual is assumed to retire at the end of age 65. Growth of portfolio is tax deferred; ending portfolio may be subject to tax. The above example is for illustrative purposes only and not indicative of any investment.